- Voice of the private banker

- Connected strategy for wealth management

- The market for private wealth

- Private wealth’s value proposition

A recent whitepaper by Alexis Calla, Sandeep Mukherjee, Nicolaj Siggelkow and Christian Terwiesch asserts that the Asian wealth management industry is currently largely analog, disconnected and lacks scale, relying on people for most aspects of the customer journey. The paper adapts the framework from a book ‘Connected Strategy‘ by two of the authors who are Wharton professors to the current wealth management industry in Asia.

We have summarised some of the content from the paper.

Wealth management is currently not scalable

There are examples of other industries such as mobility where technology has already disrupted existing incumbents. So the connected framework is a matter of strategy rather than technology.

The following chart shows the three phases of the client journey today –

- Recognise need – the client realizes the need for advice when they sell their business, or inherit or start earning much higher than they are spending

- Request the desired option – client evaluates wealth managers or investment options directly; selects one

- Respond with desired option – wealth manager responds with proposals in evaluation stage and then with a plan of action, then executes the plan

Self-directed investors rely on the wealth firm for order placement only. For advice-seeking investors, a human adviser drives most steps in the journey from client engagement, needs identification, advice generation, advice delivery, trade execution to post purchase and portfolio monitoring. The model does not scale beyond a limited number of clients per adviser. The individual adviser plays an important role through financial planning and behavioural coaching. However, the advisers have limited data-driven insights into the client, hence are prone to biases, errors and inconsistencies, for example in risk profiling. The wealth management firm has even less insight into the client as data collection and storage is fragmented.

What is a Connected Strategy

The underlying book lays out a framework for thinking about how both consumers and businesses will need to get ‘connected’ as technology gets better. The types of connected customer experiences and connection architectures are summarised in the figure.

Applying connected strategy to wealth management

Zerodha delivers its respond-to-desire experience with a broad range of investments including stocks, bonds, futures & options. Secondly, they forged a series of new connections with clients and other suppliers of knowledge through learning apps. Thirdly, they pioneered new connections with external software developers allowing a rapid expansion of relevant capabilities to its client experiences. Finally, they have expanded their offer to include a curated offer.

While private banks offer advice on investment options, they do so very manually at this stage. The research process for the long list of ‘approved funds’ as well as the selection of the short list for the clients by the investment adviser is done manually. Wealthtech firms need to be able to help clients with the search, evaluation and selection of the investment options using technology.

There is a small but growing number of wealth managers who have started to offer connected curation experiences such as DBS offering iWealth and ‘smart triggers’ for equity and FX investments. The iWealth app analyzes customer holdings and prior investment activities and then alerts customers to ideas generated by their experts, creating an information loop. Globally, Morgan Stanley has rolled out its AI-based Next Best Action engine in 2018 to drive personalised client engagement for their financial advisers. Robo-advisers provide a basic curated offering experience but their market share remains very small.

Currently, the private wealth manager’s relationship manager provides coaching informally but the value-add depends on the experience of the adviser. As wealth managers develop hybrid and fully digitized solutions, they will have to go beyond simply digitizing their existing process and create digital equivalents to the key coaching function. Behavioral sciences go beyond the utilitarian analysis of wealth management and integrate emotional and expressive benefits. They now provide many key learnings and tools that could inform and be incorporated in each step of the design and development of digital wealth management solutions and journeys.

DBS’ NAV Planner gathers data from clients, uses algorithms and heuristics to generate tailored insights to coach clients though bite-sized nudges. It is powered by more than 100 AI models, connected over 2 million clients in Singapore.

Eventually, the firm will be able to recognise client needs based on analysing the latest client and market information, decide on the relevant investment action and execute within guard-rails without any intervention, albeit complemented with continuous client communication. Australian neobank Douugh is attempting to build an automatic execution experience – automatically paying bills, making sure the client can cover them, putting money towards savings goals and investing money, and holding the client accountable to a budget. US-based Acorns does something similar.

Connected strategy can lift business efficiency

The economics of the private wealth business are a function of two variables –

- Willingness to pay – depends on perception of performance, reputation, products & services, personalization (amend this list with results from RM survey)

- Fulfilment costs – includes cost of client acquisition, the cost of engagement and advice (advisors, investment office, product management), the cost of execution (transaction platforms, operations) and functional costs (technology, compliance, support functions). The cost-to-income ratio captures fulfilment costs.

While the HNW client is willing to pay high fees, the high touch model means that the fulfilment costs are also high. The cost-to-income ratio of private wealth firms hovers around 75-80% of the fees received. Bank-based wealth management divisions have lower costs at 50-75%.

Until recently, private wealth firms were looking at technology to lower cost to income ratios. But the advent of fintech in wealth management ie robo-advisory could mean that PW needs to also look to protect its client base. While robo-advisory firms are mostly targeting mass affluent customers but could possibly encroach on the HNW segment, especially the digitally savvy millennials.

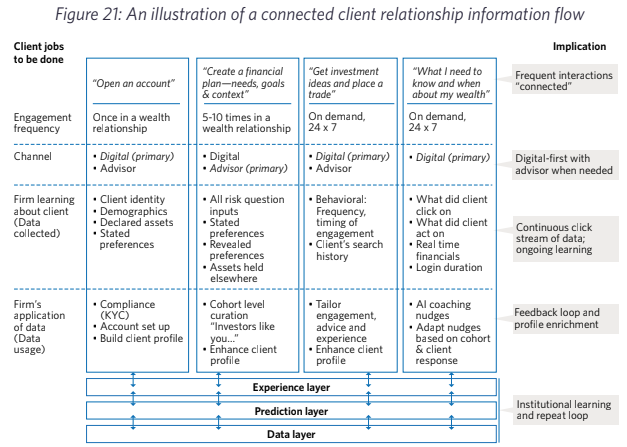

Redesigning information flows

Wealth firms need to collect much more data and organize information flows much more efficiently. However, clients are generally unwilling to give their information since they don’t see any obvious benefit and don’t have a trust-based relationship. The paper quotes a study that says clients interact with greater honesty and confidence on connected platforms in private than with an adviser. The authors contend that the ‘repeat’ dimension will allow managers to progressively collect data on clients and increase personalisation over time.

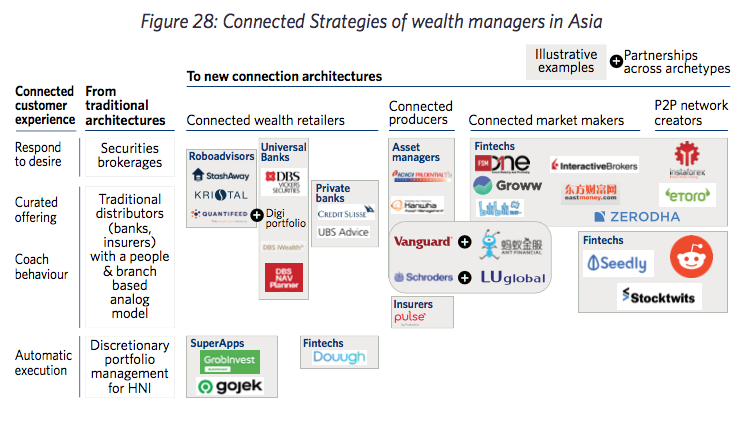

The paper runs through connected producer architectures citing examples.

Conclusion

The paper ends with several implications for wealth managers –

1. Connected wealth managers will augment their digital channel experiences and capabilities for advice and decision making, going beyond transactional convenience.

2. Connected wealth managers will redefine the role, skillset and economics of advisors.

3. The channel mix will change materially, reducing share for traditional bank-based wealth managers. A survey HNW customers in Asia said that over 90 percent would become a big tech wealth client.

4. Connected wealth managers with automated, data-driven advice capabilities will gain operating leverage and progressively reach a ‘Turing Test’ moment.

5. The industry’s ecosystem will broaden further as connected wealth managers adopt a ‘string of pearls’ partnership approach along the entire customer journey.

6. Connected wealth managers will blend skillsets and client experiences from technology-led firms with new ways of delivering unbundled, personalized solutions.

7. Connected wealth managers will partner with regulators to shape tomorrow’s rules of engagement.

You must be logged in to post a comment.