India has been wooing foreign investments, both directly as foreign direct investments (FDI) into companies as well as indirectly as ‘foreign institutional investors’ (FIIs) or ‘foreign portfolio investors’ (FPIs) into its capital markets and alternative investment funds (AIFs). FIIs already hold a significant portion of India’s listed equity market, affecting daily market fluctuations. However, the local asset management industry has been making a concerted push to get more ‘long-term capital’ into asset classes like private equity, venture capital, infrastructure etc via AIFs.

AIF managers hire placement agents to open doors, and go on extensive road-shows around the world, pitching the India story to these global investors. Often times, they end up meeting ‘gatekeepers’ called Investment Consulting (IC) firms. AIFs have to send in or upload their data into online databases that these IC firms maintain or subscribe to. And then they wait…and wait…and lament about the long lead times. It’s not clear that they realise that part of the reason investors, and their consultants, take time to decide is because they need to evaluate not only the firm that is pitching but also the India story, the asset class, and at least the top 5-10 competing asset manager firms. And that requires data standardization…which the AIF managers don’t seem to be keen on, judging by the pushback to SEBI’s recent proposal to do just that.

Before we get ahead of ourselves to explain why data standardization is necessary, let’s first look at who these IC firms are.

Defining institutional investors

Global investment consulting firms are to institutional asset owners what financial advisers are to individual investors. They provide a range of investment-related services, starting from understanding the investors’ goals, risk profile, constraints etc and advising on plan design, investment selection, execution and reporting.

But why do institutional investors need advice? Aren’t they big enough to hire enough qualified investment professionals in-house? – These are the typical questions that one mentions global investment consulting firms. So let’s back up a little and explain the context.

Just like there are many segments within the broad definition of individual investors with different needs, there are many segments within the broad umbrella of institutional investors.

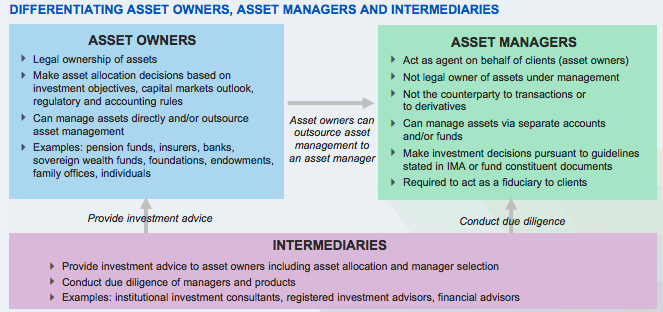

Firstly, what the Indian media tends to refer to as FII or FPI includes both asset managers as well as asset owners. It’s important to distinguish asset managers (asset management companies) such as BlackRock, Vanguard, Fidelity etc who manage money on behalf of investors, from ‘asset owners’ who are the investors.

Admittedly, asset owners, like pension funds, technically also pool their members’ money. But it’s important to note that there are different types of asset owner institutions –

- Pension funds – national, public, corporate, labour union-based, representing retirement savings of working population

- Insurance companies – statutory funds of life, health and general insurance companies, used for smoothing gains and losses from underwriting

- Corporates & Banks – treasury functions of large companies and banks, usually accumulating war chest for acquisitions

- Endowment & Foundations – pools for charitable causes, usually with very long-term horizon

- Family offices – single or multi-family, representing wealthy families and high net worth investors

- Sovereign wealth funds – government funds or investment companies, usually setting aside and investing windfalls from a natural resource with the intention of intergenerational transfer or reserve management

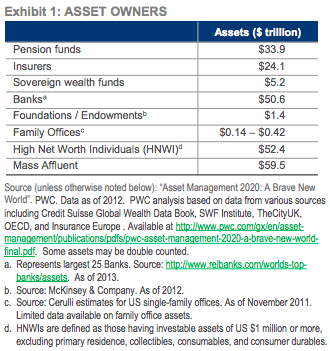

Asset owners control trillions of assets, as per the summary table below.

While it may appear that asset owner institutional investors are large enough to make their own investment decisions, this is not true. At least, it has not always been the case. The increasing complexity of the investment landscape has meant that even institutional investors seek the advice of specialists.

For example, pension funds tend to be located in one geography (country or a state within a country) and hence, may not have a global network to scout for investment opportunities around the world. Insurance companies also tend to be national. University endowments might be limited to a specific city that the university is based in. Hence, it’s reasonable that they would seek advice from specialist investment firms that have global networks.

The Indian media expects the specialist investment advice providers to be global investment banks such as JP Morgan, Goldman Sachs etc. However, these are ‘sell side’ firms with obvious conflicts of interest. They sell securities to the asset managers – so they can’t advise asset owners to select the same asset managers.

Enter the investment consultant.

Gatekeepers have evolved from pension fund consulting to OCIOs

One of the earliest type of asset owners were pension funds. Pension funds started as ‘defined-benefit’ (DB) plans i.e. the employer would promised a pre-defined retirement or pension benefit to its employees, typically a fraction of the salary at retirement date for the rest of his and his spouse’s lives. Anyone interested in the history of defined benefit plans, can read this summary – https://russellinvestments.com/-/media/files/us/insights/institutions/defined-benefit/defined-benefit-plans-a-brief-history.pdf?la=en).

The DB pension plans requires employer companies to set aside money in a separate trust to ensure it can meet its promise or liability. So the companies would ask their human resource (HR) consultants to not only help them design the benefit, but also calculate the extent of their liability. The HR consultants would hire actuaries to help with the liability calculation as it requires an estimation of retirees’ mortality rates.

Over time, these actuaries started helping the DB-plan sponsor employers not only with the liabilities, but also with advice on how to invest the assets, now sitting in a separate trust. That’s how this team, within the HR consulting firm, got to be known as ‘asset consultants’. This is how HR consulting firms like William M Mercer (now called Mercer), Towers Watson etc got into asset consulting, which is now called investment consulting.

Over time, firms with other i.e. non-HR/pension fund consulting backgrounds started offering specialist investment consulting services, hence the top 10 firms have different pedigrees.

Largest 10 investment consulting firms

The most common services provided by these major players include – _

- Plan design

- Development of investment objectives and investment policy statements

- Benchmark selection

- Operational audits

- Asset allocation advice

- Manager selection and monitoring

Source – https://www.umass.edu/preferen/You Must Read This/PickingWinners.pdf

As the trend shifted from DB corporate plans to ‘defined contribution’ (DC) platforms, the consulting firms adapted and started offering administration platforms and even fund-of-funds offerings to get economies of scale.

In the meantime, asset owners realised that they required more specialist advice in alternative asset classes like hedge funds and private equity. They started hiring a newer breed of specialist consulting firms like Albourne, Aksia etc (https://www.ipe.com/main-navigation/looking-for-alternative-advice/27375.article)

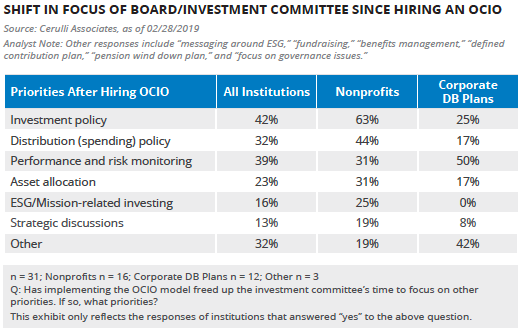

More recently the firms’ services have evolved to ‘outsourced chief investment officer’ (OCIO). The following charts have been taken from a joint study by Cerrulli Associates and BlackRock titled ‘OCIO at an inflection point’.

An often-asked question tends to be why would large institutional investors want to outsource their investment functions. Surely, they don’t want to give up power over asset manager selection. However, as the following table shows, the investment committee at asset owners still has their plates full of priorities that they rather focus on.

Interestingly, Mercer is also ranked as the largest OCIO in 2019 according to this press release (https://www.mercer.com/newsroom/mercer-global-assets-under-management-reaches-ocio-industry-milestone-by-passing-300-billion-usd.html) based on this survey (http://www.ai-cio.com/2019-Outsourced-Chief-Investment-Officer-Survey/)

ICs diversifying into implemented services such as fund-of-funds and OCIOs has become so widespread that the industry hardly has any pureplay firms (https://www.pionline.com/consultants/pure-play-consultants-become-rare-breed-amid-consolidation)

So is India finally ready for global investment consulting firms?

The largest IC firm, Mercer, actually launched in its investment consulting business in India back in 2008 (https://www.livemint.com/Money/CSszSV5ag1BXwrpmM1SGhI/Mercer-launches-investment-consulting-business-in-India.html).

But in the aftermath of the GFC, its global clients lost interest in investing in India. While Mercer did advise some of the largest local institutions such as the PFRDA on the design of the NPS, and RBI on the foreign exchange reserves (https://www.financialexpress.com/archive/mercer-likely-to-be-investment-advisor-for-forex-reserves/458751/), it concluded that the Indian institutional market wasn’t big or mature enough to warrant its stay, pulling out at the end of 2011.

Mercer’s investment consulting business, now housed within its ‘wealth’ division, has re-entered India in 2018 but has not been visible in evaluating local asset managers yet (https://www.livemint.com/Companies/X6sXty2tTtCwpE3pIXbNXN/MerceracquiresIndia-Life-Capital-in-bid-to-grow-wealth-bus.html)

Another large IC firm, Cambridge Associates, has also been sending its research staff to India for years but has not established a local presence.

Cambridge is better known than Mercer for its coverage of alternatives asset managers, so it’s natural that their name was on the short-list when SEBI mooted the proposal for setting up performance benchmarks for AIFs. That project has since been given to CRISIL.

Asset owners and their general or specialist ICs will continue to scout India for interesting investment opportunities, but it remains to be seen how many open up India offices.

You must be logged in to post a comment.