The asset management industry in India is experiencing brisk growth in assets under management driven by financialisation and expectations for further penetration into an untapped growing population. The article aims to provide an overview of the industry highlighting key trends.

MFs, dominated by equity, being challenged by AIFs

McKinsey estimated the industry’s overall AUM increased from 23 trillion rupees (~$287 billion) in 2016 to 52 trillion (~$650 billion) as of December 2020.

A Crisil report included insurance and pension assets in its estimation, sizing the industry’s AUM to be INR 135 trillion rupees (~$1687.5 billion) as at March 2022. The report attributed the significant growth to three major trends – the increasing utilization of digital platforms, a rise in investors’ risk appetite, and the availability of advisory services.

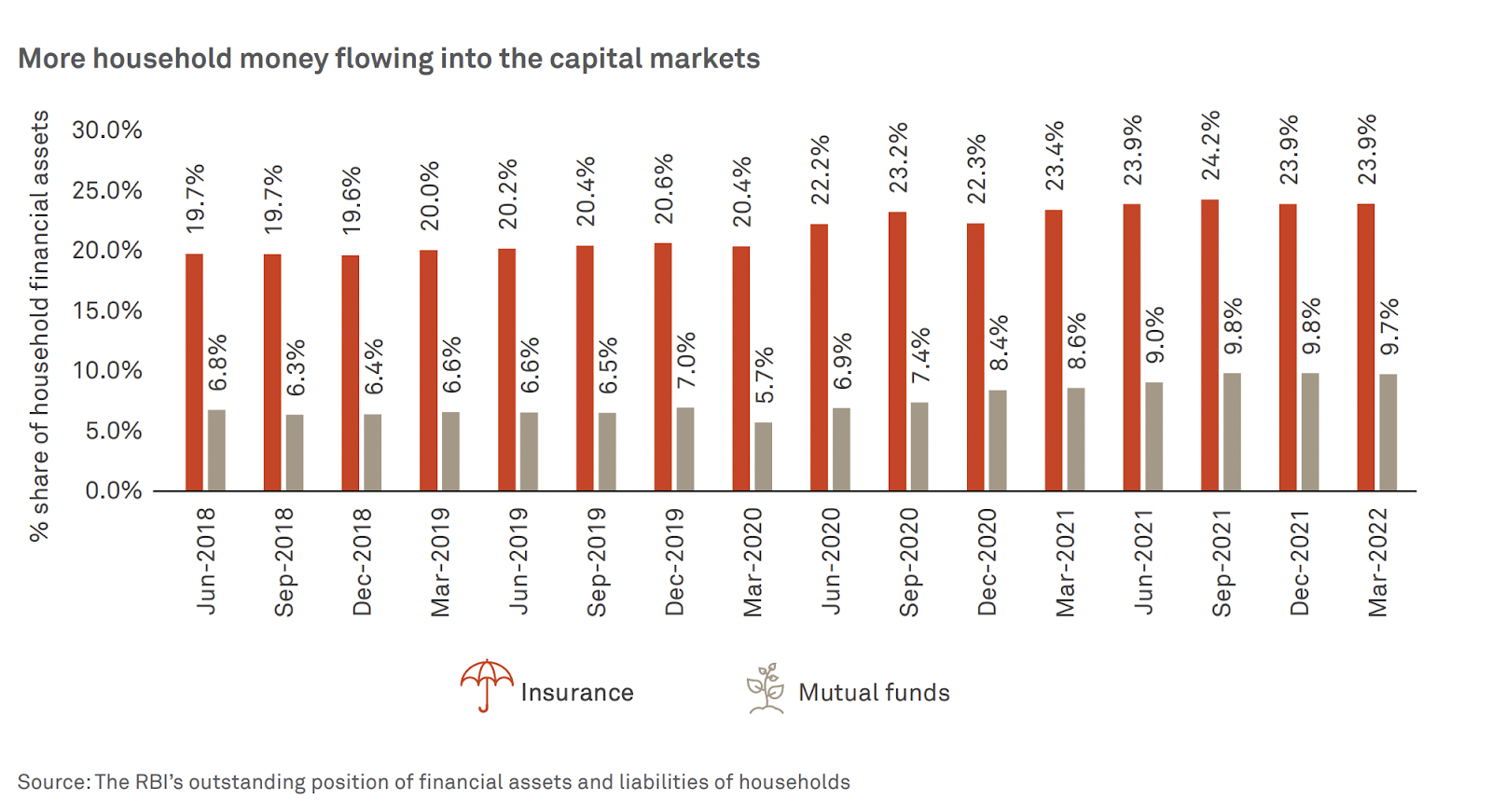

These trends have also contributed to the notable increase in the share of adults with bank accounts, which rose from 53% to 78% between 2016 and 2021, which in turn resulted in higher household savings and increased investments in capital market products such as mutual funds from 7% in 2018 to 10% in 2022.

The mutual fund segment AUM stood at 38.4 trillion rupees (~$480 billion) in April 2022, increasing to 41.53 trillion rupees (~$519.13 billion) as of March, 2023.

Industry divided on whether this constitutes low or decent penetration rates

The penetration rates in the mutual fund industry are a subject of debate, with two contrasting arguments.

The popular view is that the industry remains largely untapped. The total number of folios (accounts) is 14.57 crores (145.7 million). Based on an AMFI report, the largest share of folios is made up of retail investors.

| Breakdown of Mutual Fund Investors (%) | |

| Retail Investors | 91.10% |

| HNI | 8.20% |

| Institutions | 0.70% |

An Edelweiss report notes that the actual number of investors is only around 3.5 crore (35m), which is a small fraction compared to the country’s working-age population of over 94 crores. This indicates a significant scope for expansion within the industry.

Following a similar idea, the Crisil report suggests that the penetration rates in India remain relatively low. According to their study, while the number of folios have increased, the penetration rates in T30 and B30 cities are still low when compared to developed markets such as the United States. The report highlights limited awareness, scarcity of distributors in smaller towns, and the need for a robust intermediary system are some of the factors contributing to this trend.

Countering this argument, Nithin Kamath, the CEO of the largest broking firm Zerodha, suggests that the penetration is actually decent if one were to consider the population that earns well. His numbers are summarised in this table –

| Population | 140 crores (1140 million) |

| Number of unique demat accounts | 6 crores (60 million) |

| Number of unique MF account holders | 3.4 crores (34 million) |

His point was that one needs a minimum 2.5 lakh rupees in one’s account to be able to save and invest, hence the number of people who have sufficient funds to invest is only 10 crores out of the 140 crore Indian population. The industry target customer base is therefore approximately 10 crore people, there are approximately 3 crore unique mutual fund investors, therefore the industry’s penetration rate is about 30% which is relatively high especially for a developing economy.

| Number of People | Income( in rupees) |

| 5 crores (50 million) | < 2.5 lakhs (< $0.003 million) |

| 4.8cr (48 million) | < 5 lakhs (< $0.006 million) |

| 90 lakhs (9 million) | 5 to 10 lakhs (0.006 to 0.012 million) |

| 43 lakhs (4.3 million) | >10 lakhs (> 0.012 million) |

| Total number of potential investors is 10 crores (100 million) | |

| Number of current MF investors – 3 crores ( 30 million) = 30% penetration rate |

Larger MFs get lion’s share following Pareto principle

If we were to group the mutual fund segment by size into three buckets, the eight largest mutual fund AMCs account for approximately 75% of the industry’s total AUM. The remaining AUM is divided between medium-sized and small-sized AMCs, contributing 21% and 5% of the AUM, respectively.

| AMC Size | No. of Mutual Funds | % of Total Industry AUM |

| Large AMCs | 8 | 75% |

| Medium AMCs | 10 | 21% |

| Small AMCs | 24 | 5% |

A report by Jefferies estimates the profit pool (before tax) for the industry was 109 billion rupees ($1.36 billion), representing an average of 31 basis points of AUM. This already represents a fall of nearly 25% compared to the McKinsey estimates of around 40 bps in 2020. Jefferies estimates profit could fall further if the regulator’s proposals of performance-based fees were to go through; the proposal is being revised at the time of writing.

| FY 2022 | Rsbn | % of Avg. AUM (bps) |

| Profit before tax of all MFs | 109 | 31 |

| Expenses incurred by MFs | 308 | 88 |

Changes in distribution channels

Looking ahead, the Crisil report suggests that the asset management industry is expected to continue its growth trajectory, driven by the adoption of digital channels, increasing availability of online investment options, and improved investor experiences through technological advancements. The AUM of direct plans (without distributors) in mutual funds saw an increase from 42% to 46% between March 2017 and March 2022.

Conclusion

In conclusion, the asset management industry in India has witnessed AUM growth in various segments, with mutual funds playing a significant role. The MF industry has displayed positive financial performance and holds potential for further expansion with the adoption of digital channels and increased investor awareness expected to drive future growth in the industry.

You must be logged in to post a comment.