ISIN CODE INF251K01HQ0

Overall analysis

3-yr rolling excess returns is in the range of -7-5% and tracking error against benchmarks have been in the 4-6% range and currently it is 0%; but the funds’ performance in the short run has been deteriorating. The fund has given the maximum excess return in comparison to its peers; but has dropped to below the third line (median) over the past 1 year.

Performance analysis

Rolling returns in quartiles

The rolling return chart shows excess 3-year annualised returns in context of peer return quartiles. The blue line’s time above the third green median line indicates the fund’s better than median performance.

The rolling return chart demonstrates that the fund initially underperformed the third green median line, but from December 2019, the fund started to outperform it. The fund’s maximum rolling return is 4.38% and the minimum rolling return is -7.31%.

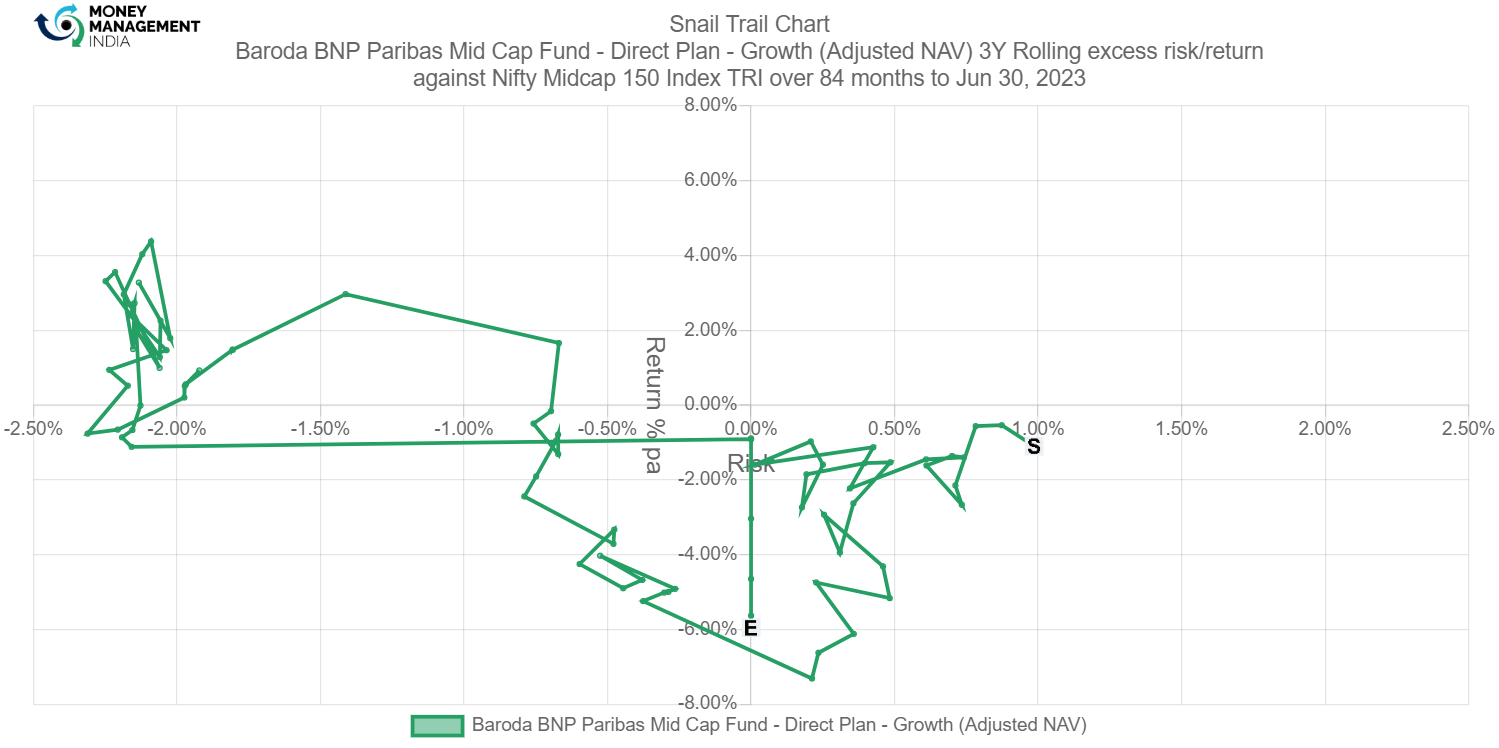

Rolling risk/return (Snail-trail)

The rolling risk/return chart shows excess 3-year annualised returns relative to the index. The top left quadrant would indicate higher returns with lower volatility than index.

Initially the fund has underperformed benchmark with relative high risk but after Jan 2020 it has outperformed benchmark with relative lower risk.

Tracking error

The tracking error chart shows how the fund ‘tracks’ against the index. The higher the TE, the more active the fund’s return has been, with the 2-4% range considered to be barely active, 4-6% range considered to be reasonably active and anything higher attributed to concentrated/focused funds. Funds with TE of less than 2% can be considered to be closet indexers.

The TE of the fund has been reasonably active from the start which is between the range 4-6% but after Oct 2022 it drastically falls to 0.

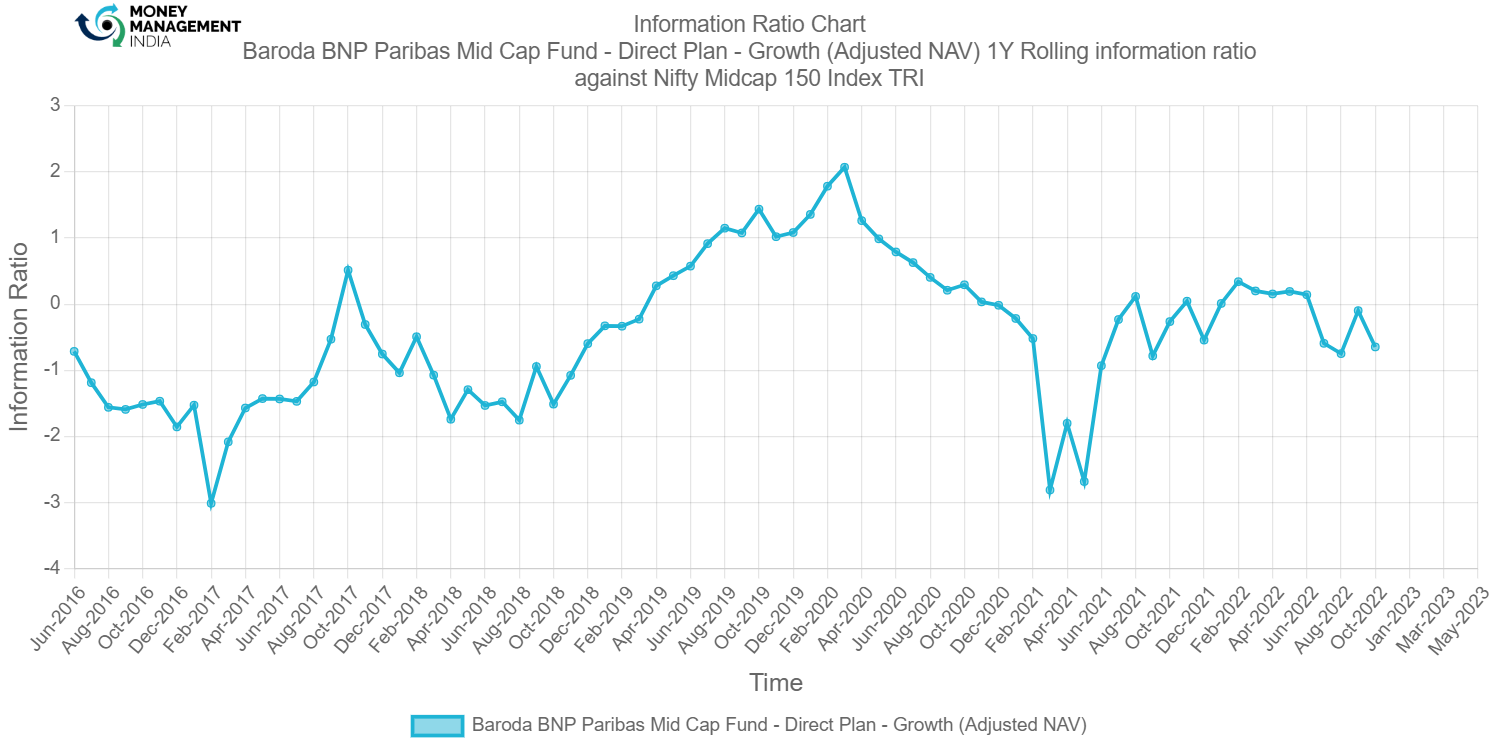

Information ratio

The information ratio is a measure of ‘risk-adjusted return’ as it’s the excess return per unit of excess volatility. Active funds should have IR of higher than 1, ideally higher than 1.3 at least to indicate skill.

The information ratio of the fund was low at the start and once it has gone above 2 but again it has come down till -2.8 in Mar 2021 which is not ideal.

Prepared by Bhavesh Mahajan, Aug 2023.

You must be logged in to post a comment.