Funds managed

| Fund name | Asset Class | License |

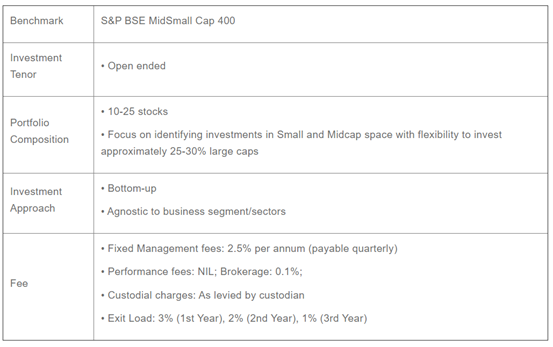

| Small and mid cap strategy | Small and Mid cap | PMS |

| Special situations value portfolio | Multi-cap | PMS |

| Pharma- wealth creator in the last cycle | PMS |

About the AMC

- Kotak PMS, one of the largest portfolio management services in India and is part of the Kotak Mahindra Group and operates under Kotak Mahindra Asset management Company.

- Kotak Group was established in 1985 by Mr. Uday Kotak.

Key staff

- Anshul Saigal, HEAD – PMS, SVP Portfolio manager

Anshul heads the Portfolio Management Services (PMS) business of KMAMC. He is an expert on value investing principles – preserving capital and generating market beating returns. Anshul has over 16 years of experience in the Indian Capital Market. He spent close to 10 years of those years with Kotak Portfolio Management Services. Prior to this, Anshul has worked with JP Morgan (Equity Research), ICICI Bank and Standard Chartered Bank, where he analysed equities and corporate credit. Anshul completed his MBA (Finance) from Management Development Institute, Gurgaon and received his Engineering degree (Industrial Engineering) from SIT, Tumkur. He is an avid reader with deep interest in behavioural finance.

- Ashish Jagnani- Equity research analyst

Ashish is an equity analyst with over 15-years of experience in the Indian Capital Markets. He was voted Equity Research Analyst in institutional investor surveys conducted by Asia Money and Asia Institutional Investor. He received this recognition during his tenure with Global Research firms – UBS and Citigroup, where he covered a wide range of sectors that interacted with global investors. Ashish is a Chartered Accountant. He has a Masters in Financial Management from Jamnalal Bajaj Institute of Management Studies.

- Aditya Joshi, CFA,CFP- Business development and Equity research analyst.

Aditya is responsible for business growth along with providing inputs on equity research. He has a total experience of 10 years in Capital Markets, the last 8 years of which he has served with the Kotak Group. He started his career in the wealth management domain and then moved onto the research side. Aditya has a Mechanical Engineer degree from Mumbai University and an MBA in Finance from KJ Somaiya Institute of Management Studies & Research, Mumbai. He is also a Certified Financial Planner (CFP) and a Chartered Financial Analyst, USA (CFA) charter-holder.

- Biren Dalal- Business development and Equity research analyst.

Biren has spent close to 12 years with Kotak Portfolio Management and Alternate Assets. He has 20 years of industry experience including that in Motilal Oswal and KRC shares and Securities. He is a Chartered Accountant with a Master of Management Studies (Finance) and Bachelor’s degree in Commerce.

Investment Philosophy (for firm)

At Kotak PMS, we believe in value Investing i.e. buying stocks at a significant discount to their current underlying value. These stocks can be out of favour and trail broad benchmarks for a period. We follow this investment style as we are confident that this approach leads to superior investment returns over the long term. We also off-set the risks and add a margin of safety by making investments in well-managed and high-quality companies, each which undergo thorough assessment and analysis before investment. Our process begins by identifying triggers as they are the catalyst to unlocking value. We use the following analytic tools and parameters:

Our process begins by identifying triggers as they are the catalysts to unlocking value. We use the following analytic tools and parameters:

- Management Quality

We assess Management Quality by analysing 3 parameters – the first, Operations Management, the second, Capital Allocation and the third, Corporate Governance.

- Operations Management: When using this parameter to assess management quality, we benchmark the company based on industry standards such as cost management, revenue growth, profitability, balance sheet leverage, etc.

- Capital Allocation: We look for companies who don’t diversify into unrelated businesses and have a history of generating at least ₹1 of market value for every ₹1 of capital retained.

- Corporate Governance: This is our prime filter in deciding whether a stock will enter our portfolio, wherein, we gauge these factors amongst many others, by meeting with managements of all our investee companies.

- Growing market opportunity

We believe that it is extremely difficult for a business to grow if its market is not growing. This situation typically leads to a turf war where competitors try to take share from each other. This is detrimental for product/ service pricing, growth or both. It is also detrimental to the interests of all incumbents.We strive to identify businesses that operate in a large and growing market space as it offers healthy participation and pricing opportunities for all players and provides space for all players to grow.

- Returns on invested capital

We use this metric to gauge the competitive strength of a company. Typically, high returns on invested capital should attract competitors but in the event that returns have been sustained over time, there would in all likelihood be certain business economics which competition cannot replicate.

- Strong financials and earnings growth

We look for businesses that have the ability to withstand vagaries of economics. Therefore, we look for businesses which have low leverage on their balance sheets, robust working capital management that is in-line with industry standards, margin structures that can withstand business volatility and earnings growth rates within a range of 15%-25%.

- Fair Valuations

We seek mispriced opportunities, where the risk-reward is favourable to us. We believe that such opportunities arise in the following distinct situations:

- Statistically cheap stocks of average companies – based on traditional valuation metrics like Discounted Cash Flows, Price to Earnings, Enterprise Value to EBITDA, etc.

- Under researched and under-appreciated opportunities – these are pockets which the general analyst community overlooks, leading to mis-pricings.

- Great companies with fair stock valuations – these are companies which have durable competitive advantages and are valued incorrectly due to temporary concerns.

Special situations value portfolio

What are special situations?

Investment operations whose results are dependent on happening or not-happening of one or more corporate events rather than market events.

Key variants:

- Price related – Securities bought at a discount to (expected) price guarantees by buyer in the form of de-listings, buy-backs, open offers, etc.

- Merger related – Shares can be created at a discount to current market price

- Corporate restructurings – Value unlocking due to corporate restructuring, assets sales, demergers, business triggers, etc.

Pharma- wealth creator in the last cycle

Pharma large caps have been the leading wealth creators of the last cycle, driven by robust US growth and high profitability in India.

Why this strategy?

Secular growth outlook, reasonably insulated across business cycles

- Penetration & US FDA compliance to drive years of growth

- Moving from simple to complex/ specialty products would provide long term opportunity of growth

Scalable Business

- Huge domestic patient population

- Globally competitive: Most global sector out of India selling in over 100 countries

Shareholder Return Business/Consumer Sector Characteristics

- High ROE

- Strong cash flows

- Low Capex

Offers a combination of stability & growth potential

Key beneficiary of the currency depreciation

- Last 1 year INR depreciated over 6% vs US Dollar

Media

Title: Can’t say about next month, but I know where to make money in next 2-3 years: Anshul Saigal, Kotak PMS, Source: ET, Date: 06 May 2019

Volatility is a friend because it offers you the right prices to buy into. If you get perturbed by volatility, you will miss out on opportunities, said Anshul Saigal, Chief Investment Officer – Kotak Portfolio Management Services.

Q. Being a small and midcap specialist in this kind of market may not be a very rewarding experience.

You have to have a thick skin to be in the markets. If you get perturbed by short-term moves in the markets, then this is not the place for you. And do not take my word for it, listen to the greats. Recently, at the Berkshire Hathaway conference and also in many of his previous notes, Warren Buffett reiterated that if you cannot take a 30% to 50% downside in equity markets, then just stay out because that can happen any time in equities.

Q.Could you give us a flavour of your top three holdings where despite 15-20% volatility, you know they would be 50-60-70% higher in the next three to five years?

I will tell you sectors in which these companies are and why we are holding them. Most of the names that we hold are names where there is some corporate action which is likely to lead to value unlocking. Because of corporate actions, these may be agnostic to market moves. Last year has been a year of immense volatility in the markets and prices have corrected.

Title: Anshul Saigal of Kotak AMC on PMS as investment option: Ticker Tv, Source; Ticker Tv, Date: 12 December 2018

PMS are products different from mutual funds. They are bottom up, as in companies which will make money for you over a complete investment cycle of 3 to 5 years.

Since you are buying stocks that disparate from the index, performance of your portfolio is also disparate. General PMS performance across the industry has beaten their respective benchmarks to the extent of 2x in many cases. We are tilted more towards capital goods, export oriented companies.

Title: Kamal Manocha engages with Anshul Saigal on Kotak Special Situations and Value PMS | PMS AIF WORLD, Source: PMS AIF world, Date: 04 June 2019

What is Kotak’s investment philosophy?

Equity investments are more of an emotional play. Markets and stock prices are volatile and they operate in their own fashion and not as per our expectations.

When one is investing in stocks, one is not investing in a ticker or a piece of paper, what one is really investing in is a business. We are looking for opportunities or value businesses wherein the value of the business is say 100 but the stock is trading at 50 or 60. Kotak makes use of the market’s mis-assessment of assets for risk adjusted return.

Three broad categories of investment.

- Investment in statistical cheap companies.

- Investing in economic moats.

- Special situations in corporate restructuring.

Demand for PMS as a product is increasing because unlike mutual funds behavior of one investor does not affect another. Where do you see PMS as a category evolving over the next 5 to 10 years?

Clients require customised accounts as per their requirement which only PMS offers. HNIs require sophisticated understanding of their portfolios. PMS will grow very much over the period of time.

Analyst questions

- You have been with Kotak for more than a decade now, how has Kotak’s investment philosophy evolved?

- Can you give us a couple of examples of stocks that you have exited and the reasons behind them?

- You have been with Kotak for more than a decade now, how has Kotak’s investment philosophy evolved?

- Can you give us a couple of examples of stocks that you have exited and the reasons behind them?

- What are some of the valuable lessons that you have learned in this industry?

You must be logged in to post a comment.