| Funds Managed | Asset Class | License |

| Small cap and mid cap | Small and mid cap | PMS |

| Pharma and healthcare | Sector fund | PMS |

| Fintech | Sector fund | PMS |

| India focus portfolio | Multicap | PMS |

About

Kotak PMS (registered under SEBI), one of the largest Portfolio Management Service providers in India, is part of the illustrious Kotak Mahindra Group and operates under the auspices of Kotak Mahindra Asset Management Company. At Kotak PMS, their focus is investing on behalf of our customers to help them achieve their personal goals and build wealth.

Key Staff

Anshul Saigal Head-PMS,

Anshul heads the Portfolio Management Services (PMS) business of KMAMC. He is an expert on value investing principles – preserving capital and generating market-beating returns. Anshul has over 20 years of experience in the Indian Capital Market. He spent close to 14 years of those years with Kotak Portfolio Management Services. Prior to this, Anshul worked with JP Morgan (Equity Research), ICICI Bank, and Standard Chartered Bank, where he analyzed equities and corporate credit. Anshul completed his MBA (Finance) from Management Development Institute, Gurgaon, and received his Engineering degree (Industrial Engineering) from SIT, Tumkur.

Ashish Jagnani – Equity research

Ashish is an equity analyst with over 15 years of experience in the Indian Capital Markets. He was voted Equity Research Analyst in institutional investor surveys conducted by Asia Money and Asia Institutional Investor. He received this recognition during his tenure with Global Research firms- UBS and Citigroup, where he covered a wide range of sectors that interacted with global investors. He is with Kotak Mahindra AMC since November 2017. Ashish is a Chartered Accountant. He has a Master’s in Financial Management from Jamnalal Bajaj Institute of Management Studies. Equity investing is his passion and he likes reading books/articles on different philosophies in investing.

Investment philosophy (for the firm)

At Kotak PMS, they believe in Value Investing i.e. buying stocks at a significant discount to their current underlying value. These stocks can be out of favor and trail broad benchmarks for a period. They follow this investment style as they are confident that this approach leads to superior investment returns over the long term. They also offset the risks and add a margin of safety by making investments in well-managed and high-quality companies, each of which undergoes a thorough assessment and analysis before investing. The process begins by identifying triggers as they are the catalyst to unlocking value. They use the following analytic tools and parameters:

The process begins by identifying triggers as they are the catalysts to unlocking value. They use the following analytic tools and parameters:

Management quality

They assess Management Quality by analyzing 3 parameters – the first, Operations Management, the second, Capital Allocation and the third, Corporate Governance.

Operations Management: When using this parameter to assess management quality, they benchmark the company based on industry standards such as cost management, revenue growth, profitability, balance sheet leverage, etc.

Capital Allocation: They look for companies that don’t diversify into unrelated businesses and have a history of generating at least ₹1 of market value for every ₹1 of capital retained.

Corporate Governance: This is their prime filter in deciding whether a stock will enter the portfolio, wherein, they gauge these factors amongst many others, by meeting with the management of all our investee companies.

Growing market opportunity

They strive to identify businesses that operate in a large and growing market space as it offers healthy participation and pricing opportunities for all players and provides space for all players to grow.

Returns on invested capital

They use this metric to gauge the competitive strength of a company. Typically, high returns on invested capital should attract competitors but in the event that returns have been sustained over time, there would in all likelihood be certain business economics that competition cannot replicate.

Strong financials and earnings growth

They look for businesses that have the ability to withstand the vagaries of economics. Therefore, look for businesses that have low leverage on their balance sheets, robust working capital management that is in line with industry standards, margin structures that can withstand business volatility, and earnings growth rates within a range of 15%-25%.

Fair valuations

They seek mispriced opportunities, where the risk-reward is favourable to us. We believe that such opportunities arise in the following distinct situations:

- Statistically cheap stocks of average companies – based on traditional valuation metrics like Discounted Cash Flows, Price to Earnings, Enterprise Value to EBITDA, etc.

- Under-researched and under-appreciated opportunities – these are pockets which the general analyst community overlooks, leading to mispricing.

- Great companies with fair stock valuations – these are companies that have durable competitive advantages and are valued incorrectly due to temporary concerns.

- Kotak Small and mid cap investment approach

Kotak PMS are “bottom-up, sector agnostic”, which means that the focus is on identifying individual companies that are undervalued based on their fundamentals, rather than investing in specific sectors or industries. This approach involves conducting in-depth research and analysis of individual companies, including their financial statements, management teams, and competitive positioning.

The portfolio composition of the Kotak PMS strategy consists of 10-25 stocks, with a focus on small-cap companies The investment tenor is open-ended, which means that investors can enter and exit the strategy at any time. The benchmark for the strategy is the Nifty Small Cap 100.

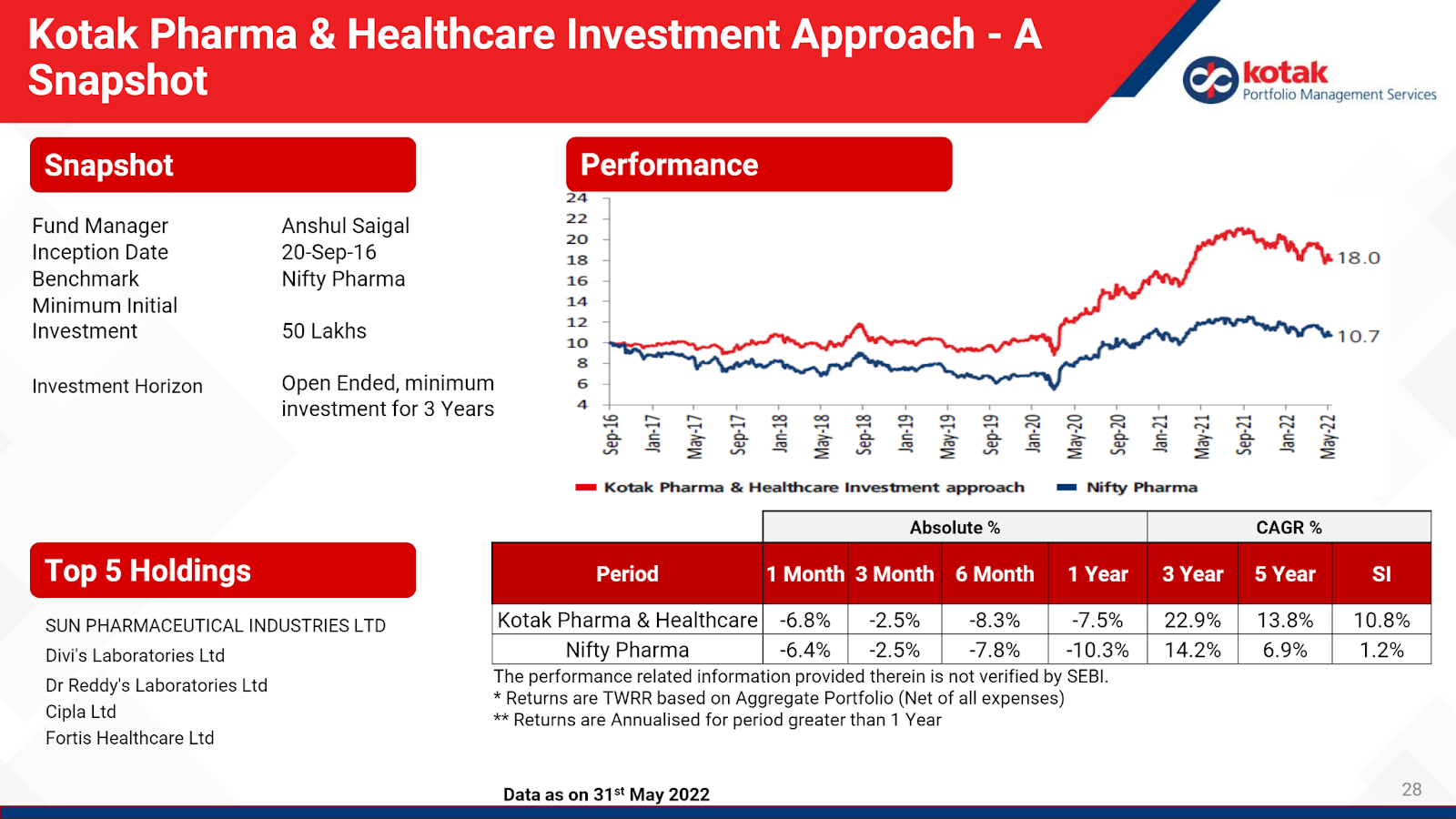

b). Kotak Pharma and healthcare investment approach

The investment objective of the approach is to generate capital appreciation by investing in equities with a medium to long-term perspective. The approach will primarily invest in all equity and equity-related instruments, with an emphasis on capturing available opportunities in the pharma and healthcare-related stocks.

The strategy of the approach is to focus on investing in companies that operate in the pharma and healthcare sectors. These companies may include pharmaceutical manufacturers, biotech firms, medical device companies, healthcare providers, and other related businesses. The equity style box for the investment approach is in the value category and also in the mid and small-size categories; it suggests that the approach focuses on investing in mid-sized and small-sized companies that are undervalued by the market.

c). Kotak fintech investment approach

Based on the information provided, Kotak FinTech’s investment approach is focused on a unique portfolio positioning that includes a concentrated portfolio of approximately 20 stocks, with a mix of quality Banks, NBFCs, Insurance (BFSI), and Technology stocks.

The portfolio is positioned to take advantage of the secular growth of the IT sector, which is being accelerated by COVID-led disruptions and the transformation to the cloud, adoption of AI, machine learning, and new technologies. The banks, NBFCs, and insurance sectors were impacted by the pandemic, but the worst is believed to be behind them, and recovery is expected to follow.

Overall, the portfolio is positioned to provide a quality investment opportunity, offering an estimated 20% earnings CAGR over FY22-24E, with a 20-21% FY23 ROE, according to Bloomberg estimates. The IT stocks in the portfolio are expected to offer a 12-13% EPS CAGR, and 4.4% FCF with ROEs of 27%, while the BFSI stocks are expected to offer an average 27-30% earnings CAGR with ROEs of 15-16%.

The portfolio composition is designed to help reduce volatility on the downside, with technology stocks providing a cushion, while financial stocks are expected to benefit from the post-COVID macro recovery.

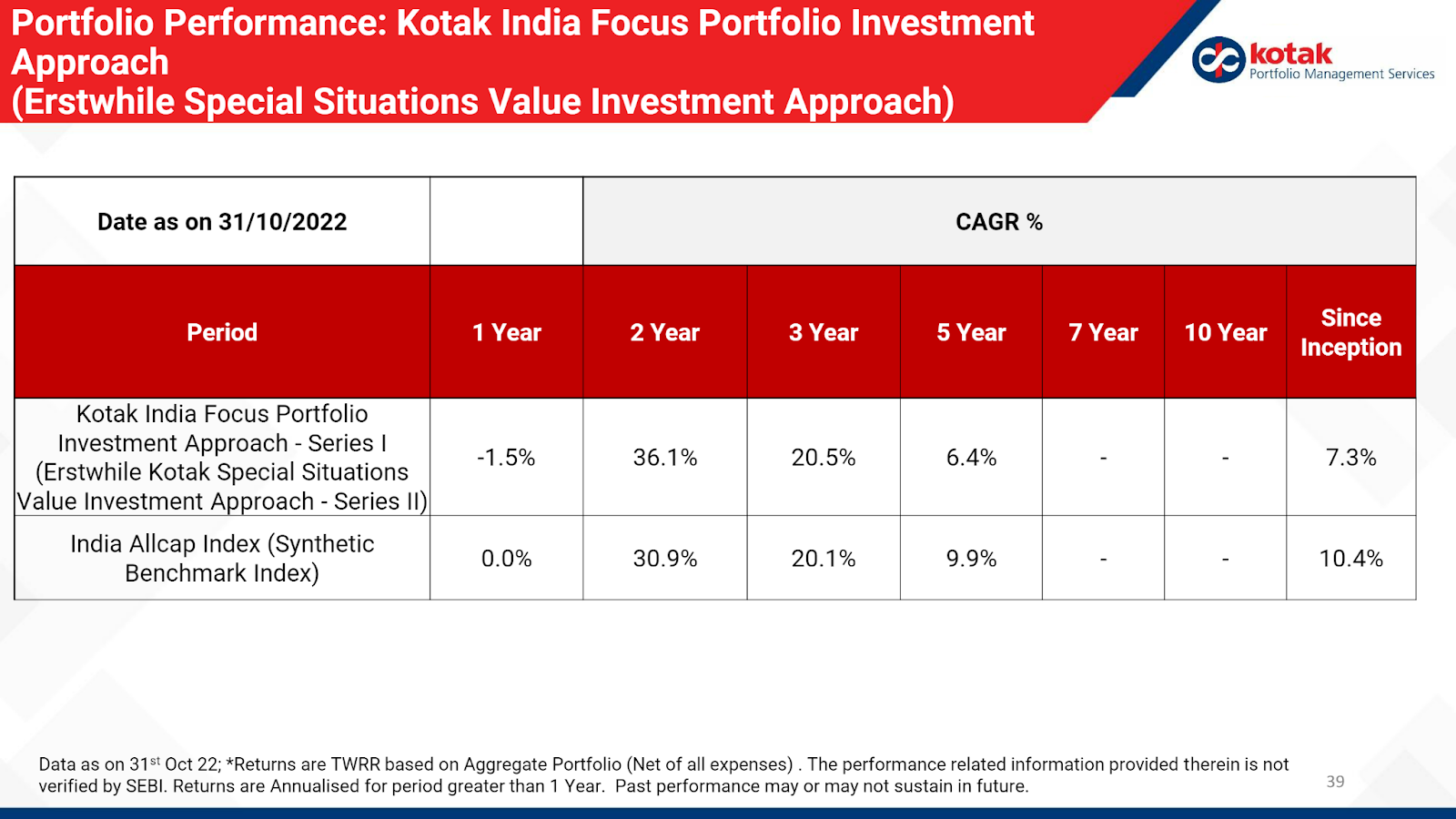

d.)Kotak India focus portfolio investment approach

At Kotak Portfolio Managers, the approach to value investing involves thinking of stocks as fractional ownership in a business, rather than just ticker symbols. The focus is on identifying businesses with sustainable competitive advantages and strong earnings potential. The key is to find companies where growth is not fully priced in, rather than simply seeking absolute cheapness. The valuation multiples are less relevant in this approach.

A key focus of this approach is to prevent permanent capital loss by seeking a margin of safety and investing in good quality businesses that have consistent earnings. The portfolio is typically concentrated, and the downside risk is capped by the strength of the underlying businesses.

Media

Is Growth Relevant for Value Investing – Kotak PMS | Anshul Saigal | Vikas Agrawal

Anshul Saigal explains that there is an inverse trade-off between the cost of funds and the multiples that companies get. If the cost of funds is low, the multiples are high, and if the cost of funds goes up, the multiples are relatively lower. The speaker notes that currently, there are multiple uncertainties in the market, but one certainty is that interest rates are going up due to high inflation. The markets have already priced in significant upside and growth, and there is no room in multiples for them to go up. This means that there will either be a time correction or a price correction. The speaker addresses a follow-up question about whether the BJP government was capable enough to deal with the inflation issue, as it seems to have gone out of control. The speaker argues that compared to the average inflation rate during the period of 2009 to 2014, which was 10-10.5%, today’s inflation rate of 7.5% is relatively better. Furthermore, the current inflation rate is lower than that of the US, which is experiencing an inflation rate of 8.6%. The speaker suggests that lack of experience in managing inflation has worked for the government as they have managed inflation better than in the past.

What is value investing?

Value investing is a strategy where investors buy stocks that are trading below their intrinsic value or what they are worth. The goal of value investing is to buy quality businesses at reasonable prices to ensure the preservation of capital and generate consistent returns. The premise of value investing is that good businesses will eventually appreciate in value and generate returns for investors over time.

In personal investments, people have different options for investing their capital, such as savings accounts, fixed deposits, bonds, and equities. While fixed deposits and bonds offer relatively lower returns, equities offer higher returns but also carry higher risks. Similarly, investors look for companies that offer higher returns than other investment options, and this is where value investing comes into play.

When investing in a business, an investor wants to earn more than they would from a fixed deposit or a bond, and they expect a return on their capital that is higher than their personal investments. Therefore, a good business should generate a return on capital that is higher than the investor’s personal investments.

The two main factors that determine whether a business is a good investment are quality and price. A quality business is one that generates high returns on capital, grows consistently over time, and has a competitive advantage over its peers. An investor wants to pay a reasonable price for such a business. Value investors look for quality businesses that are available at reasonable prices.

While quality businesses command a premium, growth is not always priced in. Sometimes, businesses with temporary problems become available at reasonable valuations, presenting opportunities for value investors to buy quality businesses at a discount. However, investors need to be careful while selecting these businesses to ensure that they are not buying low-quality businesses that appear cheap.

The speaker from Kotak AMC says that they have been managing PMS (portfolio management services) since 2012. They have two flagship portfolios, the Special Situations and Value Strategy and the Small and Mid Cap Strategy, with a 10-year track record. The Small and Mid-Cap Strategy has generated 18% compounded returns and a 5-6% alpha over the index, while the Special Situations Strategy has generated 15% compounded returns and a 5-6% alpha over the benchmark. They also have two sectoral portfolios, Pharma and Health Care, and Fintech, which have performed well against their respective benchmarks.

The speaker says that their success is due to their disciplined approach to identifying sector leaders and companies with strong balance sheets and growth trajectories. They hold companies that are by and large debt-free, and they anticipate 25-26% compounded earnings growth between FY 21 and 24 with a PE ratio of 17 times. They hold roughly 36-37% large caps and an equivalent amount of small caps, with the remaining being mid caps. They hold some cash and deploy capital in a staggered manner, usually over a month. They make changes to the portfolio only when necessary and have a long-term investment approach.

PMS portfolios typically consist of 20 to 25 stocks and are more concentrated than mutual funds which may hold 60 to 70 stocks. This concentration allows for greater flexibility in making changes to the portfolio based on individual client needs, such as holding onto stocks that have appreciated significantly in value for existing clients but not buying them for new clients. Additionally, PMS portfolios can deploy capital over a period of time rather than all at once and can modulate the portfolio to reflect changing market conditions or individual client needs. Overall, PMS portfolios offer a different flavor and product compared to mutual funds and can be a valuable tool for investors looking for more flexibility and customization in their investment strategies.

You must be logged in to post a comment.