Funds managed

| Fund name | Asset class/ Market cap allocation | License |

| Girik Multicap Growth Equity Strategy | Multi-Cap Equity | PMS |

| Girik Deep Value Strategy | Large in equity, Some in Liquid funds for liquidity purpose | PMS |

About

Founded in 2009, Girik Capital is a Mumbai based SEBI registered portfolio manager providing discretionary asset management services. PMS Reg. No. : PM/INP000003369

Their focus is Indian listed equities and they cater to corporates, institutions, family offices and individuals from India and globally. The investment management team at Girik brings more than 20 years of cumulative experience in investment management.

They believe investing does not have to be complicated and they keep it that way. They screen investment opportunities based on strict parameters such as Growth, Quality and competitive advantage.

Their Profit/(Loss) after tax till now: 6,37,00,000 rupees ( As on March 31, 2020)

Source: From disclosure document under financial performance

Key staff

Charandeep Singh, Founder, Principal officer and fund manager

Charandeep currently jointly leads the investment decision making process at Girik. He has over two decades of experience in capital markets.

Charandeep’s experience includes more than 10 years of investing in India, prior to which he was with Lehman Brothers as a Director in the investment banking division, global leveraged finance group, based in New York and London.

He holds a Diploma in Accounting & Finance from the London School of Economics and Political Science (1999) and is a Master in Finance from London Business School (2002). Linkedin

Varun Daga, Founder and fund manager

Varun is co-founder of Girik and jointly leads the investment decision-making process. He is a self-taught successful investor and has a remarkable experience of over a decade in capital markets.

Varun has developed proprietary systems and screeners in order to identify promising leading growing companies well in advance of their biggest gains. Prior to Girik, he ran the equity investment division at his family office.

He holds a Bachelor of Management Studies, majoring in finance from Narsee Monjee College of Economics. Linkedin

Funds managed

Girik Multicap Growth Equity Strategy

Inception Date: 03 December, 2009

Number of Stocks: 21

AUM size: 450 ( in Cr. Approx.)

Benchmark: Nifty 50

Fund manager expense: 2%

Exit load :

1st year 3%

2nd year 3%

3rd year 3%

Disclaimer: Returns as of 28th Feb, 2021, Returns up to 1 year are absolute and above 1 year are CAGR.

Source: https://app.pmsaifworld.com/pms-details

Source: https://girikcap.com/performance.aspx

2) Girik Deep value strategy

Investment Objective: The primary investment objective of the Portfolio Manager is to generate capital appreciation over a period of time.

Description of Securities : Underlying securities would be listed equities. Investments in liquid funds/fixed term papers will be made for liquidity purposes.

Basis of selection of such types of securities as part of the investment approach : The portfolio will concentrated around value stocks which offer a compelling upside over a 5 years horizon.

Benchmark: Nifty 50

Indicative tenure or investment horizon : Girik Deep Value Strategy looks to achieve capital appreciation over the long term. It requires a gestation of minimum 5 years in order for the investment manager to be able to maximize strategy performance.

Fees Structure on boarding of clients either directly or through empanelled distributor :

Fixed Management Fees upto 2.50% per annum of daily average AUM

Performance based fees upto to 30% of portfolio return (with or without hurdle rate)

Performance based fees is calculated subject to Higher Water Marking Principle

Performance based fees will be charged at the end of the financial year or at the close of account, whichever is earlier. In case of interim contribution / withdrawals by clients, performance based fees shall be charged on a proportionate basis

Terms of Redemption:

For exit within Year 1 from the date of activation of account – 3%

For exit within Year 2 from the date of activation of account – 2%

For exit within Year 3 from the date of activation of account – 1%

Investment Philosophy ( for the firm)

At Girik, their philosophy is inspired by William O Neil’s CANSLIM style of investment management to primarily invest in leading, high quality, high growth businesses that are run by honest and capable management teams.

Investment style

They buy growth stocks at a reasonable price which is expensive in the short run but cheap in the long run. Whatever the premium is built in, it needs a serious justification.

Their investment strategy is CANSLIM

CANSLIM, created by Investor’s Business Daily William J. O’Neil, is a system for selecting growth stocks using a combination of fundamental and technical analysis techniques.

Steps are discussed in the investment process.

Investment process

They follow a five step process which includes identifying leading companies from a leading industry, looking at company fundamentals, valuations, and risk management framework.

Step 1

Automated Screening For Superior Outcomes – Industry strength, Relative price strength, Earnings acceleration.

Industry Strength

- Industry strength relative to other industries

- Shortlist leading stocks in leading industries

- 50% of a stock performance tied to the industry group

Relative Price Strength

- Look for leading price performers

- 52 week and lifetime highs

- Winners show price strength early in a bull cycle

Earnings Acceleration

- Stable historical earnings

- Accelerating current annual & quarterly earnings

- Immense future earnings growth potential

Step 2

Establishing Leadership

- Product/ Service Leadership

- Ability to Scale

- Management Track Record

- Efficient Capital Allocation & Superior Return Ratios

- Governance Standards & Alignment of Interest.

Step 3

Fundamental Research Overview – Business model, Financial metrics, Governance

Business Model

- Product / service leadership

- Market size & opportunity

- Management efficiency – superior execution & delivery

- Relevance to all stakeholders

Financial Metrics

- Superior return ratios

- Efficient use of capital

- Healthy free cash flow generation

- Funding of growth ideally through internal accruals

- Low to no debt

Governance

- No significant related party transactions

- Minority shareholder friendly (E.g. – Dividends, Buybacks)

- Alignment of interests – management compensation & ESOPs

- Ideally no large promoter pledges and sales in the past

- Professionally managed; genuine board of directors;

Step 4

Valuation Consideration

Value in Growth

- Expensive in the short run but cheap in the long run

- Accelerating earnings growth combined with leadership ensures premium multiple justification

Margin of Safety

- Assessment of longevity of growth and leadership

- Estimate downside risk of going wrong due to overestimating growth… Star point.. How do you measure it?

Traditional Valuation Metrics

- Reliance on traditional valuation metrics can be deceiving

- Trading Multiples (P/CF, P/E, EV/EBITDA) relative to historical averages – significant premium requires serious justification

- “Low P/E” investing can be a value trap

Step 5

Risk Management Framework – Portfolio review, Eliminating losers, Taking profits

Portfolio Review

- Weekly fundamental stock reviews

- Ensure balance in portfolios based on industry & stock concentration, market cap weights, and liquidity

- Check for technical / distribution patterns

Eliminating Losers

- Identify and eliminate investment mistakes actively

- Monitor for any sectorial and stock weakness

- No averaging down on a loss making position

Taking Profits

- Riding winners until see earnings growth deceleration

- Selling in euphoric tops … Does it mean tactical asset allocation

- Red flags – crowded trades, consensus bets, excessive media coverage, over-guidance from management

Source: https://girikcap.com/Investment-Philosophy.aspx

Investment process: (Concise way)

- Screening companies based in “price strength” using proprietary screeners

- Leading stocks in leading industries

- Combination of sharp earnings momentum and value

- Establish business leadership and competitive edge

- History of growth, quality, execution and value creation

- Strong governance practices, management structures and alignment of interest

- Look for “value in growth” but try not to overpay for growth

- Ability to multiply in size and command premium valuations

- Establish margin of safety through assessment of longevity or growth and leadership

- Eliminating “losers” in portfolios upon establishment of change in business fundamentals

The seven criteria that comprise CANSLIM are as follows:

- C: Current quarterly earnings per share (EPS) has increased sharply from the same quarters’ earnings reported in the prior year. Generally, investors using CANSLIM want EPS growth of over 20%, but the higher the better.

- A: Annual earnings increases over the last five years. Again, annual EPS growth should ideally be in excess of 20% over the last three to five years.

- N: New products, management, or new events/information that push the company’s stock to new highs. This type of headline news can cause short-term excitement, propelling a surge of optimism within the market, and subsequent price appreciation.

- S: Scarce supply coupled with a strong appetite for a stock creates excess demand—and an environment in which share prices can soar. Companies acquiring (re-purchasing) their own stock reduces market supply and can indicate an expectation of increased demand, along with insider confidence in the firm.

- L: Laggard stocks are preferred within the same industry. Use the relative strength index (RSI) as a guide. The RSI is a momentum indicator that measures the magnitude of price changes to determine whether the price of a stock or asset is overbought or oversold. The RSI ranges from zero to 100. An RSI reading below 30 suggests that the stock is oversold and could be undervalued—creating a buying opportunity (bullish). Conversely, an RSI reading of above 70 signifies that a stock could be overbought or overvalued and could be a chance to sell (bearish).

- I: Pick stocks that have institutional sponsorship by a few institutions with recent above-average performance. For example, this could be a recently public company, still supported by a small handful of well known private equity firms. Be cautious of stocks that are over-owned by institutions as you want to get in before the big money is fully invested.

- M – Determine market direction by reviewing market averages daily. A market average measures the overall price level of a given market, as defined by a specified group of stocks, such as the Dow Jones Industrial Average. CANSLIM stocks tend to be over-performers in bull markets. Source

Media

Keep Emotions Out of Investing’ says Girik Capital, Feb 8, 2021

Excerpts from the video is shared in the below article

Keep aside emotions, be process-oriented while making investment decisions: Charandeep Singh, ET, Feb 8, 2021

Charandeep singh has shared his opinion on how P/E multiple has been driven & how market reacts to it. Then he explained their firm stock picking process which is systematic, fundamentally and price oriented. In order to overcome the biases he mentioned make sure the process works and build awareness that a process is followed and not falling in a trap.

Get over your own fears and don’t sell your winner too soon, Varun Daga, ET, Feb 8, 2021

Varun Daga shared his experience and learnings with Bajaj finance which is a multibagger of the last decade. He spoke about how a multibagger can be made with the right temperament and by balancing the emotions. He shared his view on recency bias where a lot of investors get trapped which results in missing the biggest rallies. But their idea is to become aware of it, overcome it by sticking to their process.

Analyst questions

Business Management assessment

Firm has a good experience as they are in the business for more than 10 years with two fund managers one is young and dynamic and other is extremely experienced, AUM size is relatively very huge of INR 450 crores. Good thing about the company is they are in accumulated profit of INR 6 crores till now

Investment assessment

Since the inception of the fund, they have generated a phenomenal alpha return of 10.61% . Their style is GARP (Growth at reasonable price) which focuses on Multi-cap equity with a concentrated portfolio of some 20 odd stocks.

Product assessment

Exit load is relatively higher which is 3% for the first three years. This is recommended for Investors who have an investment horizon of more than 3 years.Fund manager expense is with industry standard of 2% every year.

Quant assessment

The return of the fund since inception is 20.31% which is for almost 11 odd years, be it 10 year, 7 year, or 5 year time horizon, this fund has done a great performance in the past with more than 20% in all the specified time horizon.

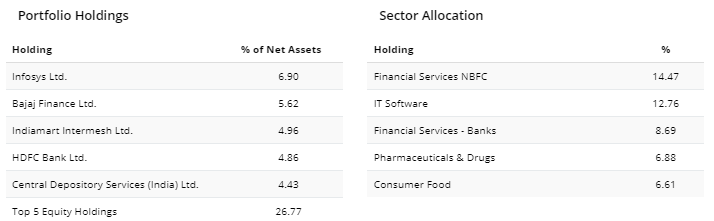

Top 5 holdings – Infosys, Bajaj Finance, Indiamart Intermesh, HDFC Bank, Certral Depository Services.

- What inefficiency do you spot from the market and how do you exploit it?

- What made you follow CANSLIM approach to pick stocks?

- Can you talk about the process which helps you to overcome the confirmatory and recency biases?

- On what basis do you pre-screen the stocks from the whole universe?

- How do you assess the industry strength?

- What are all the industries do you think will outperform in the next 3-5 years?

- You have mentioned “Reliance on traditional valuation metrics can be deceiving” what are those and what valuation techniques do you follow to find the intrinsic value of a stock?

- You have been outperforming the market a lot of times since inception, so what’s your alpha target for next few years?

- Why do you hold a significant amount of cash in the portfolio? Do you use it as a tactical basis?

Prepared by Subramanian K

Peer review

Date: 31st March

You must be logged in to post a comment.